888 BOT #alerts█ 888 BOT #alerts (open source)

This is an Expert Advisor 'EA' or Automated trading script for ‘longs’ and ‘shorts’, which uses only a Take Profit or, in the worst case, a Stop Loss to close the trade.

It's a much improved version of the previous ‘Repanocha’. It doesn`t use 'Trailing Stop' or 'security ()' functions (although using a security function doesn`t mean that the script repaints) and all signals are confirmed, therefore the script doesn`t repaint in alert mode and is accurate in backtest mode.

Apart from the previous indicators, some more and other functions have been added for Stop-Loss, re-entry and leverage.

It uses 8 indicators, (many of you already know what they are, but in case there is someone new), these are the following:

1. Jurik Moving Average

It's a moving average created by Mark Jurik for professionals which eliminates the 'lag' or delay of the signal. It's better than other moving averages like EMA , DEMA , AMA or T3.

There are two ways to decrease noise using JMA . Increasing the 'LENGTH' parameter will cause JMA to move more slowly and therefore reduce noise at the expense of adding 'lag'

The 'JMA LENGTH', 'PHASE' and 'POWER' parameters offer a way to select the optimal balance between 'lag' and over boost.

Green: Bullish , Red: Bearish .

2. Range filter

Created by Donovan Wall, its function is to filter or eliminate noise and to better determine the price trend in the short term.

First, a uniform average price range 'SAMPLING PERIOD' is calculated for the filter base and multiplied by a specific quantity 'RANGE MULTIPLIER'.

The filter is then calculated by adjusting price movements that do not exceed the specified range.

Finally, the target ranges are plotted to show the prices that will trigger the filter movement.

Green: Bullish , Red: Bearish .

3. Average Directional Index ( ADX Classic) and ( ADX Masanakamura)

It's an indicator designed by Welles Wilder to measure the strength and direction of the market trend. The price movement is strong when the ADX has a positive slope and is above a certain minimum level 'ADX THRESHOLD' and for a given period 'ADX LENGTH'.

The green color of the bars indicates that the trend is bullish and that the ADX is above the level established by the threshold.

The red color of the bars indicates that the trend is down and that the ADX is above the threshold level.

The orange color of the bars indicates that the price is not strong and will surely lateralize.

You can choose between the classic option and the one created by a certain 'Masanakamura'. The main difference between the two is that in the first it uses RMA () and in the second SMA () in its calculation.

4. Parabolic SAR

This indicator, also created by Welles Wilder, places points that help define a trend. The Parabolic SAR can follow the price above or below, the peculiarity that it offers is that when the price touches the indicator, it jumps to the other side of the price (if the Parabolic SAR was below the price it jumps up and vice versa) to a distance predetermined by the indicator. At this time the indicator continues to follow the price, reducing the distance with each candle until it is finally touched again by the price and the process starts again. This procedure explains the name of the indicator: the Parabolic SAR follows the price generating a characteristic parabolic shape, when the price touches it, stops and turns ( SAR is the acronym for 'stop and reverse'), giving rise to a new cycle. When the points are below the price, the trend is up, while the points above the price indicate a downward trend.

5. RSI with Volume

This indicator was created by LazyBear from the popular RSI .

The RSI is an oscillator-type indicator used in technical analysis and also created by Welles Wilder that shows the strength of the price by comparing individual movements up or down in successive closing prices.

LazyBear added a volume parameter that makes it more accurate to the market movement.

A good way to use RSI is by considering the 50 'RSI CENTER LINE' centerline. When the oscillator is above, the trend is bullish and when it is below, the trend is bearish .

6. Moving Average Convergence Divergence ( MACD ) and ( MAC-Z )

It was created by Gerald Appel. Subsequently, the histogram was added to anticipate the crossing of MA. Broadly speaking, we can say that the MACD is an oscillator consisting of two moving averages that rotate around the zero line. The MACD line is the difference between a short moving average 'MACD FAST MA LENGTH' and a long moving average 'MACD SLOW MA LENGTH'. It's an indicator that allows us to have a reference on the trend of the asset on which it is operating, thus generating market entry and exit signals.

We can talk about a bull market when the MACD histogram is above the zero line, along with the signal line, while we are talking about a bear market when the MACD histogram is below the zero line.

There is the option of using the MAC-Z indicator created by LazyBear, which according to its author is more effective, by using the parameter VWAP ( volume weighted average price ) 'Z-VWAP LENGTH' together with a standard deviation 'STDEV LENGTH' in its calculation.

7. Volume Condition

Volume indicates the number of participants in this war between bulls and bears, the more volume the more likely the price will move in favor of the trend. A low trading volume indicates a lower number of participants and interest in the instrument in question. Low volumes may reveal weakness behind a price movement.

With this condition, those signals whose volume is less than the volume SMA for a period 'SMA VOLUME LENGTH' multiplied by a factor 'VOLUME FACTOR' are filtered. In addition, it determines the leverage used, the more volume , the more participants, the more probability that the price will move in our favor, that is, we can use more leverage. The leverage in this script is determined by how many times the volume is above the SMA line.

The maximum leverage is 8.

8. Bollinger Bands

This indicator was created by John Bollinger and consists of three bands that are drawn superimposed on the price evolution graph.

The central band is a moving average, normally a simple moving average calculated with 20 periods is used. ('BB LENGTH' Number of periods of the moving average)

The upper band is calculated by adding the value of the simple moving average X times the standard deviation of the moving average. ('BB MULTIPLIER' Number of times the standard deviation of the moving average)

The lower band is calculated by subtracting the simple moving average X times the standard deviation of the moving average.

the band between the upper and lower bands contains, statistically, almost 90% of the possible price variations, which means that any movement of the price outside the bands has special relevance.

In practical terms, Bollinger bands behave as if they were an elastic band so that, if the price touches them, it has a high probability of bouncing.

Sometimes, after the entry order is filled, the price is returned to the opposite side. If price touch the Bollinger band in the same previous conditions, another order is filled in the same direction of the position to improve the average entry price, (% MINIMUM BETTER PRICE ': Minimum price for the re-entry to be executed and that is better than the price of the previous position in a given %) in this way we give the trade a chance that the Take Profit is executed before. The downside is that the position is doubled in size. 'ACTIVATE DIVIDE TP': Divide the size of the TP in half. More probability of the trade closing but less profit.

█ STOP LOSS and RISK MANAGEMENT.

A good risk management is what can make your equity go up or be liquidated.

The % risk is the percentage of our capital that we are willing to lose by operation. This is recommended to be between 1-5%.

% Risk: (% Stop Loss x % Equity per trade x Leverage) / 100

First the strategy is calculated with Stop Loss, then the risk per operation is determined and from there, the amount per operation is calculated and not vice versa.

In this script you can use a normal Stop Loss or one according to the ATR. Also activate the option to trigger it earlier if the risk percentage is reached. '% RISK ALLOWED' wich is calculated according with: '%EQUITY ON EACH ENTRY'. Only works with Stop Loss on 'NORMAL' or 'BOTH' mode.

'STOP LOSS CONFIRMED': The Stop Loss is only activated if the closing of the previous bar is in the loss limit condition. It's useful to prevent the SL from triggering when they do a ‘pump’ to sweep Stops and then return the price to the previous state.

█ ALERTS

There is an alert for each leverage, therefore a maximum of 8 alerts can be set for 'long' and 8 for 'short', plus an alert to close the trade with Take Profit or Stop Loss in market mode. You can also place Take Profit limit and Stop Loss limit orders a few seconds after filling the position entry order.

- 'MAXIMUM LEVERAGE': It is the maximum allowed multiplier of the % quantity entered on each entry for 1X according to the volume condition.

- 'ADVANCE ALERTS': There is always a time delay from when the alert is triggered until it reaches the exchange and can be between 1-15 seconds. With this parameter, you can advance the alert by the necessary seconds to activate it earlier. In this way it can be synchronized with the exchange so that the execution time of the entry order to the position coincides with the opening of the bar.

The settings are for Bitcoin at Binance Futures (BTC: USDTPERP) in 15 minutes.

For other pairs and other timeframes, the settings have to be adjusted again. And within a month, the settings will be different because we all know the market and the trend are changing.

Wyszukaj w skryptach "take profit"

Ampleforth Rebase MACDThis script reveals Ampleforth rebase levels which are going to always work. In addition to that is MACD crossovers serving as potential buy/sell entries. You can set alerts for MACD crossovers and price entering balanced value area (0.96 - 1.06).

MACD signals can be used to automatically open a position and entering a balanced value area can be used as take-profit. Since the price will always move to this level, using this strategy without leverage should be profitable.

Ampleforth seems like a nice asset to trade since it is unlikely to correlate with anything else. At least not when it gets to the extreme levels.

MACD+ Strategy [SystemAlpha]This is a strategy based on MACD Oscillator . Instead of using just the normal crossovers, we use trend filters, trailing stop loss and take profit targets. This strategy was developed for crypto, forex and stocks on daily timeframe but feel free to experiment on 15 minutes or higher using heikin ashi or normal candles

In this strategy you have a choice of:

Trend Filters:

- Average Directional Index ( ADX ) – buy when price is trend is up and sell when trend is down.

- Moving Average (MA) – buy when price close above the defined moving average and sell when price close below moving average

- Parabolic SAR – buy when SAR is above price is above price and sell when SAR is below price.

- All - Use ADX , MA and SAR as filters

For MA Filter , you can use the “TF MA Type” and "TF MA Period" parameter to select Simple or Exponential Moving Average and length.

Stop Loss:

- Average True Range (ATR) – ATR % stop as trailing stop loss.

- Parabolic SAR ( SAR ) – Parabolic SAR adapted as trailing stop loss.

For ATR , you can use the “ATR Trailing Stop Multiplier” parameter to set an initial offset for trailing stop loss.

Take Profit Target:

- Average True Range (ATR) – ATR % stop as trailing stop loss.

- Standard % – Percent as target profit

For ATR , you can use the “ATR Take Profit Multiplier” parameter to set an initial offset for trailing stop loss.

Additional feature include:

- Regular and Hidden Divergence display and alerts

STRATEGY ONLY:

- Set back test date range

- Set trade direction - Long, Short or Both

- Use timed exit - Select method and bars

- Method 1: Exit after specified number of bars.

- Method 2: Exit after specified number of bars, ONLY if position is currently profitable.

- Method 3: Exit after specified number of bars, ONLY if position is currently losing.

TradingView Links:

Alerts:

MACD:

How to use:

1. Apply the script by browsing through Indicators --> Invite-Only scripts and select the indicator

2. Once loaded, click the gear (settings) button to select/adjust the parameters based on your preference.

3. Wait for the next BUY or SELL signal to enter the trade!

Disclaimer:

The indicator and signals generated do not constitute investment advice; are provided solely for informational purposes and therefore is not an offer to buy or sell a security; are not warranted to be correct, complete or accurate; and are subject to change without notice.

Grid Like StrategyIt is possible to use progressive position sizing in order to recover from past losses, a well-known position sizing system being the "martingale", which consists of doubling your position size after a loss, this allows you to recover any previous losses in a losing streak + winning an extra. This system has seen a lot of attention from the trading community (mostly from beginners), and many strategies have been designed around the martingale, one of them being "grid trading strategies".

While such strategies often shows promising results on paper, they are often subjects to many frictions during live trading that makes them totally unusable and dangerous to the trader. The motivations behind posting such a strategy isn't to glorify such systems, but rather to present the problems behind them, many users come to me with their ideas and glorious ways to make money, sometimes they present strategies using the martingale, and it is important to present the flaws of this methodology rather than blindly saying "you shouldn't use it".

Strategy Settings

Point determines the "grid" size and should be adjusted accordingly to the scale of the symbol you are applying the strategy to. Higher value would require larger price movements in order to trigger a trade, as such higher values will generate fewer trades.

The order size determines the number of contracts/shares to purchase.

The martingale multiplier determines the factor by which the position size is multiplied after a loss, using values higher to 2 will "squarify" your balance, while a value of 1 would use a constant position sizing.

Finally, the anti-martingale parameter determines whether the strategy uses a reverse martingale or not, if set to true then the position size is multiplied after any wins.

The Grid

Grid strategies are commons and do not present huge problems until we use certain position sizing methods such as the martingale. A martingale is extremely sensitive to any kind of friction (frictional costs, slippage...etc), the grid strategy aims to provide a stable and simple environment where a martingale might possibly behave well.

The goal of a simple grid strategy is to go long once the price crossover a certain level, a take profit is set at the level above the current one and stop loss is placed at the level below the current one, in a winning scenario the price reach the take profit, the position is closed and a new one is opened with the same setup. In a losing scenario, the price reaches the stop loss level, the position is closed and a short one is opened, the take profit is set at the level below the current one, and a stop loss is set at the level above the current one. Note that all levels are equally spaced.

It follows from this strategy that wins and losses should be constant over time, as such our balance would evolve in a linear fashion. This is a great setup for a martingale, as we are theoretically assured to recover all the looses in a losing streak.

Martingale - Exponential Decays - Risk/Reward

By using a martingale we double our position size (exposure) each time we lose a trade, if we look at our balance when using a martingale we see significant drawdowns, with our balance peaking down significantly. The martingale sequence is subject to exponential growth, as such using a martingale makes our balance exposed to exponential decays, that's really bad, we could basically lose all the initially invested capital in a short amount of time, it follows from this that the theoretical success of a martingale is determined by what is the maximum losing streak you can endure

Now consider how a martingale affects our risk-reward ratio, assuming unity position sizing our martingale sequence can be described by 2^(x-1) , using this formula we would get the amount of shares/contracts we need to purchase at the x trade of a losing streak, we would need to purchase 256 contracts in order to recover from a losing streak of size 9, this is enormous when you take into account that your wins are way smaller, the risk-reward ratio is totally unfair.

Of course, some users might think that a losing streak of size 9 is pretty unlikely, if the probability of winning and losing are both equal to 0.5, then the probability of 9 consecutive losses is equal to 0.5^9 , there are approximately 0.2% of chance of having such large losing streak, note however that under a ranging market such case scenario could happen, but we will see later that the length of a losing streak is not the only problem.

Other Problems

Having a capital large enough to tank 9any number of consecutive losses is not the only thing one should focus on, as we have to take into account market prices and trading dynamics, that's where the ugly part start.

Our first problem is frictional costs, one example being the spread, but this is a common problem for any strategy, however here a martingale is extra sensitive to it, if the strategy does not account for it then we will still double our positions costs but we might not recover all the losses of a losing streak, instead we would be recovering only a proportion of it, under such scenario you would be certain to lose over time.

Another problem are gaps, market price might open under a stop-loss without triggering it, and this is a big no-no.

Equity of the strategy on AMD, in a desired scenario the equity at the second arrow should have been at a higher position than the equity at the first arrow.

In order for the strategy to be more effective, we would need to trade a market that does not close, such as the cryptocurrency market. Finally, we might be affected by slippage, altho only extreme values might drastically affect our balance.

The Anti Martingale

The strategy lets you use an anti-martingale, which double the position size after a win instead of a loss, the goal here is not to recover from a losing strike but instead to profit from a potential winning streak.

Here we are exposing your balance to exponential gross but you might also lose a trade at the end a winning streak, you will generally want to reinitialize your position size after a few wins instead of waiting for the end of a streak.

Alternative

You can use other-kind of progressions for position sizing, such as a linear one, increasing your position size by a constant number each time you lose. More gentle progressions will recover a proportion of your losses in a losing streak.

You can also simulate the effect of a martingale without doubling your position size by doubling your target profit, if for example you have a 10$ profit-target/stop-loss and lose a trade, you can use a 20$ profit target to recover from the lost trade + gain a profit of 10$. While this approach does not introduce exponential decay in your balance, you are betting on the market reaching your take profits, considering the fact that you are doubling their size you are expecting market volatility to increase drastically over time, as such this approach would not be extremely effective for high losing streak.

Conclusion

You will see a lot of auto-trading strategies that are based on a grid approach, they might even use a martingale. While the backtests will look appealing, you should think twice before using such kind of strategy, remember that frictional costs will be a huge challenge for the strategy, and that it assumes that the trader has an important initial capital. We have also seen that the risk/reward ratio is theoretically the worst you can have on a strategy, having a low reward and a high risk. This does not mean that progressive position sizing is bad, but it should not be pushed to the extreme.

It is nice to note that the martingale is originally a betting system designed for casino games, which unlike trading are not subject to frictional costs, but even casino players don't use it, so why would you?

Thx for reading

inwCoin Martingale Strategy ( for Bitcoin )** Same as my previous martingale script but this version = opensource **

inwCoin Martingale Strategy is the proof of concept strategy that in the end, anyone who using martingale strategy will kaboom their portfolio.

For those who don't know what is "martingale".. it's a simple double down strategy in the hope to cover the loss in previous entry.

Example

In the game that if you win, you'll get 100% of your bet money back.

1st loss = 1$

2nd loss = bet 2$ : if win, get 2$ / real profit = 1$ ( 2-1 )

3rd loss = bet 4$ : if win, get 4$ / real profit = 1$ ( 4 - ( 2+1) )

4th loss = bet 8$ : if win, get 8$ / real profit = 1$ ( 8 - ( 4+2+1 ) )

...

...

10th loss = bet 512$ : if win, get 512$ / real profit = 1$ ( 512 - ( 256+128+64+32+16+8+4+2+1) )

as you can see, the next bet will be first bet x 2^(n-1)

and the profit will equal to your first bet.

==================

In trading and forex EA ( Expert Advisor or bot ) people use this strategy to fool newbies that their martingale system will generate steady income for eternity.

But in reality, this strategy will destroy your whole portfolio eventually some time in the future. Because there will be some "Blackswan event" in market at some point in time. And one who ignore this fact, will lose everything.

But, if you using low risk strategy and generate some profit from your low-risk portfolio. You can take small chunk of that profit and put it in riskier strategy like this martingale, to accerelate your profit snowball.

===================

Parameter Explaination

====================

Price = datasource for indicator calculation

Fixed position size option = if uncheck, the "Start position size" parameter will be % of your initial capital. If checked, it will fixed position size ( like 1 BTC )

Start Position Logic = condition to enter first trade

- MACD singal > 0 : Self explanatory, default macd value

- Stochastic RSI cross up : enter when sto line cross up from bottom ( 20 )

- ATR channel : enter trade if price cross above 2.3 ATR

Take Profit Percent = take profit target % from average entry

Start martingale ..= if price compare to average position entry less than this %, it will start to double down ( martingale )

Martingale Multiplier = you can specific how big you'll double down, default is 2

Trade Direction = long only for now

Use date rang = self explanatory

** make sure to setup your initial capital in properties tab **

On chart

=======

White Line = Average position price

Orange Line = your current equity

If equity less than 0, it will close any remaining positions ( It's mean your position got liquidated )

If price > equity line for "take profit percent" it will close any remaining positions.

=======

As you can see, this strategy survive 2018 drop and pump profit to 1000+% ( Check in the strategy tester tab > list of trades )

But in May 2020 -50% drop in just 3 days, your whole portfolio got liquidated.

Actually, after some digging in profit and backtest result.

This strategy, when it can survive a shape drop, can generate a lot of profit.

So, if you want to use martingale. Make sure to use only small chunk of your profit from "low-risk" strategy to accelerate your profit generation ( aka degen port )

DO NOT greedy and use all of your initial capital or borrowed money to use with this strategy!

BEST Trailing Stop StrategyHello traders

Here we go again.... with the second strategy snippet.

Reminder: the first snipper was a Trailing Profit strategy script

What's on the menu?

A trailing stop is designed to protect gains by enabling a trade to remain open and continue to profit as long as the price is moving in the investor's favor.

The order closes the trade if the price changes direction by a specified percentage or dollar amount.

Trigger me I'm famous

I developed many trading strategies in my career and often I've been asked to trigger a trailing-stop once a certain % move has been made.

On the screenshot below, the SL trigger is plotted in maroon.

Once the price goes past that level for the first time, I'll start trailing the trailing stop level.

In other words, when we see a price makes an interesting move in percentage value - we decide to trail the stop for at least not losing any more

All the BEST

Dave

TradingView Alerts to MT4 MT5 + dynamic variables NON-REPAINTINGAccidentally, I’m sharing open-source profitable Forex strategy. Accidentally, because this was aimed to be purely educational material. A few days ago TradingView released a very powerful feature of dynamic values from PineScript now being allowed to be passed in Alerts. And thanks to TradingConnector, they could be instantly executed in MT4 or MT5 platform of any broker in the world. So yeah - TradingConnector works with indices and commodities, too.

The logic of this EURUSD 6h strategy is very simple - it is based on Stochastic crossovers with stop-loss set under most recent pivot point. Setting stop-loss with surgical precision is possible exactly thanks to allowance of dynamic values in alerts. TradingConnector has been also upgraded to take advantage of these dynamic values and it now enables executing trades with pre-calculated stop-loss, take-profit, as well as stop and limit orders.

Another fresh feature of TradingConnector, is closing positions only partly - provided that the broker allows it, of course. A position needs to have trade_id specified at entry, referred to in further alerts with partial closing. Detailed spec of alerts syntax and functionalities can be found at TradingConnector website. How to include dynamic variables in alert messages can be seen at the very end of the script in alertcondition() calls.

The strategy also takes commission into consideration.

Slippage is intentionally left at 0. Due to shorter than 1 second delivery time of TradingConnector, slippage is practically non-existing. This can be achieved especially if you’re using VPS server, hosted in the same datacenter as your brokers’ servers. I am using such setup, it is doable. Small slippage and spread is already included in commission value.

This strategy is NON-REPAINTING and uses NO TRAILING-STOP or any other feature known to be faulty in TradingView backtester. Does it make this strategy bulletproof and 100% success-guaranteed? Hell no! Remember the no.1 rule of backtesting - no matter how profitable and good looking a script is, it only tells about the past. There is zero guarantee the same strategy will get similar results in the future.

To turn this script into study so that alerts can be produced, do 2 things:

1. comment “strategy” line at the beginning and uncomment “study” line

2. comment lines 54-59 and uncomment lines 62-65.

Then add script to the chart and configure alerts.

This script was build for educational purposes only.

Certainly this is not financial advice. Anybody using this script or any of its parts in any way, must be aware of high risks connected with trading.

Thanks @LucF and @a.tesla2018 for helping me with code fixes :)

Directional Movement Index with double exponential moving averagThe Directional system is a trend-following method developed by J. Welles Wilder,

in the mid-1970s. It identifies trends and shows

when a trend is moving fast enough to make it worth following. It helps traders to

profit by taking chunks out of the middle of important trends.

Trading Rules

1. Trade only from the long side when the positive Directional line is above the

negative one. Trade only from the short side when the negative Directional line

is above the positive one. The best time to trade is when the ADX is rising, show-

ing that the dominant group is getting stronger.

2. When ADX declines, it shows that the market is becoming less directional. There

are likely to be many whipsaws. When ADX points down, it is better not to use

a trend-following method.

3. When ADX falls below both Directional lines, it identifies a flat, sleepy mar-

ket. Do not use a trend-following system but get ready to trade, because major

trends emerge from such lulls.

4. The single best signal of the Directional system comes after ADX falls below

both Directional lines. The longer it stays there, the stronger the base for the

next move. When ADX rallies from below both Directional lines, it shows that

the market is waking up from a lull. When ADX rises by four steps

from its lowest point below both Directional lines, it “rings a bell” on a

new trend . It shows that a new bull market or bear market is being

born, depending on what Directional line is on top.

5. When ADX rallies above both Directional lines, it identifies an overheated mar-

ket. When ADX turns down from above both Directional lines, it shows that the

major trend has stumbled. It is a good time to take profits on a directional trade.

If you trade large positions, you definitely want to take partial profits.

This particular version uses DEMA (double exponential moving averages) in attempt to catch moves sooner.

Trade Manager (Open Source Version)Hello my young padawans looking for the FORCE to get richer on your next trade

I got pinged at least three times today asking where the hell is the indicator of the day. You asked, I delivered :)

Here's your free open-source Trade Manager Version. My associates might kill me for sharing that one... anyway this is a real GIFT.

I won't share such quality indicators too often for FREE so hope you'll appreciate its value. It can really help with your day to day trading (on top of making your charts looking more awesome)

This is an even better version compared to my previous Trade Manager Trade-Manager . It's basically a standalone version, meaning you'll have to update with 2 lines your own indicator and follow my educational post from yesterday (pasted it below also) to learn how to do it

Please read this educational post I published for you before proceeding further : How-to-connect-your-indicator-with-the-Trade-Manager

From here you normally connected the data source of your own indicator to the Trade Manager. If not, here's a reminder of the article mentionned above

Step 1 - Update your indicator

For the screenshot you see above, I used this indicator : Two-MM-Cross-MACD/ . "But sir are you really advertising your other indicators here ??" ... hmmm.... YES but I gave them for free so ... stop complaining my friend :)

Somewhere in the code you'll have a LONG and a SHORT condition. If not, please go back to study trading for noobs (I'm kidding !!!)

So it should look to something similar

nUP = ma_crossover and macd_crossover

nDN = ma_crossunder and macd_crossunder

What you will need to add at the very end of your script is a Signal plot that will be captured by the Trade Manager. This will give us :

// Signal plot to be used as external

// if crossover, sends 1, otherwise sends -1

Signal = (nUP) ? 1 : (nDN) ? -1 : na

plot(Signal, title="Signal")

The Trade Manager engines expects to receive 1 for a bullishg signal and -1 for bearish .

Step 2 - Add the Trade Manager to your chart and select the right Data Source

I feel the questions coming so I prefer to anticipate :) When you add the Trade Manager to your chart, nothing will be displayed. THIS IS NORMAL because you'll have to select the Data Source to be "Signal"

Remember our Signal variable from the Two MM Cross from before, now we'll capture it and.....drumb rolll...... that's from that moment that your life became even more AWESOME

The Engine will capture the last signal from the MM cross or any indicator actually and will update the Stop Loss, Take Profit levels based on the parameters you set on the Trade Manager

It should work with any indicator as long as you're providing a plot Signal with values 1 and -1 . In any case, you can change the Trade Manager you'll find a better logic for your trading

Now let's cover the different parameters of the tool

It should be straightforward but better to explain everything here

+Label lines : if unchecked, no SL/TPs/... will be displayed

+Show Stop Loss Signal : Will display the stop loss label. You have the choice between three options :

By default, the Stop Loss is set to NONE. You'll have to select a different option to enable the Stop Loss for real

++Percentage : Will set the SL at a percent distance from the price

++Fixed : SL fixed at a static price

++Trailing % : Trailing stop loss based on percentage level

The following is a KEY feature and I got asked for it many times those past two days. I got annoyed of getting the same request so I just did it

++Trailing TP: Will move the Stop Loss if the take profit levels are hit

Example: if TP1 is hit, SL will be moved to breakeven. If TP2 is hit, SL will be moved from TP1 to TP2

+Take Profit 1,2,3 : Visually define the three Take Profit levels. Those are percentage levels .

Meaning if you set TP1 = 2, it will set the TP1 level 2% away from the entry signal

Please note that once a Take profit level is reached, it will magically disappear. This is to be expected

I'll share in the future a way more complete version with invalidation, stop loss/take profits based on indicator, take profit based on supports/resistances, ...

I believe is such a great tool because can be connected to any indicator. I confess that I tried it only with a few... if you find any that's not working with the Trade manager, please let me know and I'll have a look

PS

I want to give a HUUUUUUUGE shoutout to the PineCoders community who helped me finishing it

Wishing you all the best and a pleasant experience with my work

David

Peak Valley Estimation StrategyIntroduction

Its the first strategy that i post here, so don't expect ground breaking stuff, when testing my indicators i always used prorealtime and not tradingview. This strategy use signals generated by the peak/valley estimator indicator i posted long ago, i think the signals generated where sometimes quite accurate in some markets thus providing potential material for a profitable strategy.

The indicator use 3 parameters, therefore the optimisation process is not easy, but i selected what i judged good parameters values at first glance. The strategy is in its more simple form without stop or anything, the detection of peaks and valley can allow for tighter stops since we expect the price to reverse, but take into account that sops and take profits are parameters subject to optimization process except if selected with strict money management rules and not profit optimization.

Of course trading the strategy in this form is far from being great, if we take into account the market non stationarity then we might expect loss during trending markets. Trend strength indicators could help switch from a reversal to breakout strategy thus maybe providing more control.

I really hope you find an use for the strategy.

Notes

Its been three long years since i started tradingview, and i put more efforts in my indicators than in my studies and life overall, this have created complicated situations and i can't afford to follow up with this, therefore i announce that in the end of june i will leave tradingview for quite a long time, at least until i have my degree. I announce it in advance in case some of you want helps of any kind. I will post all the indicators, both in progress and finished i have made during those three years. I hope you can all understand.

Thanks for reading !

makeTPSo this model try to use the the take profit issue as important

the model is based on the early model that I put in last publication , the problem is that the fire point of the buy and sell has a delay and shoot some bars after (its not repaint but a bug due to TV code) . but once it stay it will calculate correctly the take profits . so I add take profit 1 and take profit 2 to the script . and since take profit 1 is correct without delay I add option to use it as buy again or short again . you can the older entry point which is H= high or L =low as your initial buy point but be aware that it sometime shoot too late since the problem in TV script to transfer the price correctly .or to enter to buy again option which is based on take profit 1 . the H and L are correctly detecting most of the time the Highs and the lows so by going on the trend them you can use the TP which are by % to max out your gains .. this is the theory behind this model

see here on amazon the concept

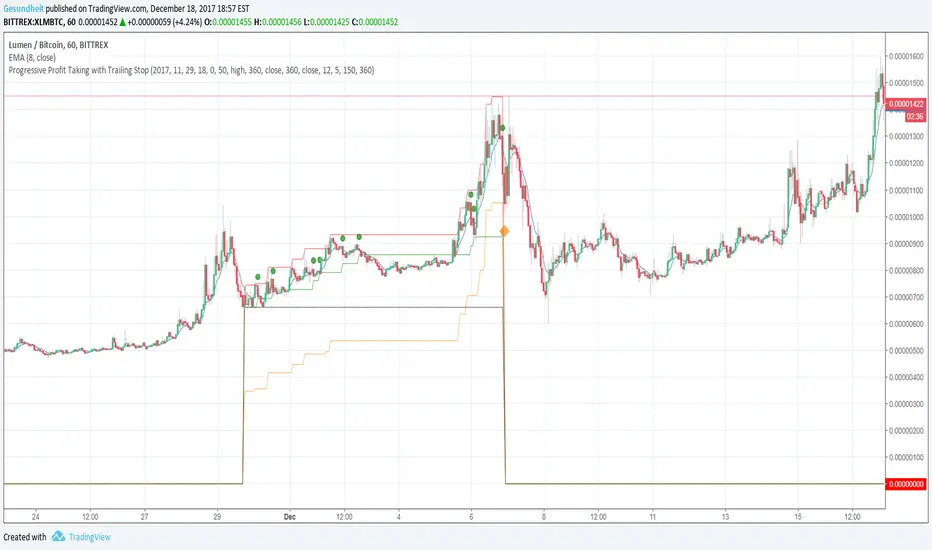

Progressive Profit Taking with Trailing StopThis is version 2 of

Special features:

Added partial profit taking as price rises. Profit taking is triggered by price crossing an EMA.

After profit taking, price has to rise by a user-specified percent before taking profits again.

Also includes condition for fully closing position after meeting specified profit target.

To incorporate into your algo, turn the plotshape functions into alertcondition.

Golden Cross, SMA 200 Moving Average Strategy (by ChartArt)This famous moving average strategy is very easy to follow to decide when to buy (go long) and when to take profit.

The strategy goes long when the faster SMA 50 (the simple moving average of the last 50 bars) crosses above the slower SMA 200. Orders are closed when the SMA 50 crosses below the SMA 200. This simple strategy does not have any other stop loss or take profit money management logic. The strategy does not short and goes long only!

Here is an article explaining the "golden cross" strategy in more detail:

www.stockopedia.com

On the S&P 500 index (symbol "SPX") this strategy worked on the daily chart 81% since price data is available since 1982. And on the DOW Jones Industrial Average (symbol "DOWI") this strategy worked on the daily chart 55% since price data is available since 1916. The low number of trades is in both cases not statistically significant though.

All trading involves high risk; past performance is not necessarily indicative of future results. Hypothetical or simulated performance results have certain inherent limitations. Unlike an actual performance record, simulated results do not represent actual trading. Also, since the trades have not actually been executed, the results may have under- or over-compensated for the impact, if any, of certain market factors, such as lack of liquidity. Simulated trading programs in general are also subject to the fact that they are designed with the benefit of hindsight. No representation is being made that any account will or is likely to achieve profits or losses similar to those shown.

Elder's Market Thermometer [LazyBear]Market temperature, introduced by Dr.Alexander Elder, helps differentiate between sleepy, quiet and hot market periods.

Following is Mr.Elder's explanation on how to use this indicator (from his book "Come in to my Trading Room"):

"When markets are quiet, the adjacent bars tend to overlap. The consensus of value is well established, and the crowd does little buying or selling outside of yesterday’s range. When highs and lows exceed their previous day’s values, they do so only by small margins. Market Thermometer falls and its EMA slants down, indicating a sleepy market. When a market begins to run, either up or down, its daily bars start pushing outside of the previous ranges. The histogram of Market Thermometer grows taller and crosses above its EMA, which soon turns up, confirming the new trend."

"Market Thermometer gives four trading signals, based on the relationship between its histogram and its moving average:

1) The best time to enter new positions is when Market Thermometer falls below its moving average. When Market Thermometer falls below its EMA, it indicates that the market is quiet. If your system flashes an entry signal, try to enter when the market is cooler than usual. When Market Thermometer rises above its moving average, it warns that the market is hot and slippage more likely.

2) Exit positions when Market Thermometer rises to triple the height of its moving average. A spike of Market Thermometer indicates a runaway move. When the crowd feels jarred by a sudden piece of news and surges, it is a good time to take profits. Panics tend to be short-lived, offering a brief opportunity to cash in. If the EMA of Market Thermometer stands at 5 cents, but the Thermometer itself shoots up to 15 cents, take profits. Test these values for the market you are trading.

3) Get ready for an explosive move if the Thermometer stays below its moving average for five to seven trading days. Quiet markets put amateurs to sleep. They become careless and stop watching prices. Volatility and volume fall, and professionals get a chance to run away with the market. Explosive moves often erupt from periods of inactivity.

4) Market Thermometer can help you set a profit target for the next trading day. If you are a short-term trader and are long, add the value of today’s Thermometer EMA to yesterday’s high and place a sell order there. If you are short, subtract the value of the Thermometer’s EMA from yesterday’s low and place an order to cover at that level."

You can configure the "Explosive Move threshold" (default: 3), "Idle Market Threshold" (default: 7) and "Thermometer EMA length" (default: 22) via Options page.

More info:

"Come in to my Trading Room - A complete Guide to Trading" by Dr.Alexander Elder. (Page 162)

List of my other indicators:

- Chart:

- GDoc: docs.google.com

Grok/Claude Quantum Signal Pro V2 * Grok/Clause X Series📊 Quantum Signal Pro+ Enhanced - Complete Guide

🎯 What This Script Does

This is an advanced momentum reversal trading system that combines multiple technical filters to identify high-probability buy and sell signals. It's designed to catch market reversals at extreme oversold/overbought levels while avoiding choppy, low-conviction trades.

🔍 Buy/Sell Signal Logic

BUY SIGNAL (Long Entry)

A BUY signal triggers when ALL core conditions are met:

Core Requirements (Always Required):

ADX Trending - Market must be trending (ADX > 20 by default)

RSI Oversold - RSI below 30 (extreme selling)

Fisher Oversold - Fisher Transform below -2.0 (momentum exhaustion)

Optional Filters (Can be toggled ON/OFF):

EMA Trend Alignment - Price must be above 50 EMA (uptrend confirmation)

Volume Surge - Volume must be 1.5x above average (strong participation)

Divergence Confirmation - Regular or Hidden bullish divergence detected

Signal Philosophy: Wait for extreme oversold conditions in a trending market, then enter when momentum exhausts.

SELL SIGNAL (Short Entry)

A SELL signal triggers when ALL core conditions are met:

Core Requirements (Always Required):

ADX Trending - Market must be trending (ADX > 20)

RSI Overbought - RSI above 70 (extreme buying)

Fisher Overbought - Fisher Transform above 2.0 (momentum exhaustion)

Optional Filters (Can be toggled ON/OFF):

EMA Trend Alignment - Price must be below 50 EMA (downtrend confirmation)

Volume Surge - Volume must be 1.5x above average

Divergence Confirmation - Regular or Hidden bearish divergence detected

Signal Philosophy: Wait for extreme overbought conditions in a trending market, then enter when momentum exhausts.

🛠️ Key Settings Explained

Dynamic Bands Settings

Basis Type: EMA (faster) or SMA (smoother)

Basis Length: 20 (default) - The midline

ATR Period: 14 - Volatility measurement window

ATR Multiplier: 2.5 - Band width (higher = wider bands)

Adaptive Band Width: ON - Bands widen in trending markets (ADX-based)

💡 Tip: Keep ATR multiplier at 2.5-3.0 for most markets. Lower values (1.5-2.0) for ranging markets.

Signal Filters (The Brain)

Fisher Transform

Period: 10 bars

Overbought: +2.0

Oversold: -2.0

More sensitive than RSI, catches momentum shifts faster

RSI (Relative Strength Index)

Period: 14 bars

Oversold: 30

Overbought: 70

Classic momentum indicator

ADX (Trend Strength)

Length: 14

Threshold: 20

Purpose: Filters out choppy/ranging markets

ADX < 20 = Ranging (no signals)

ADX > 20 = Trending (signals allowed)

💡 Critical Tip: ADX is your signal quality filter. Raise threshold to 25-30 for cleaner signals in volatile markets.

EMA Trend Filter (Optional - OFF by default)

Period: 50 bars

When ON: Only buys above EMA, only sells below EMA

Use case: Strong trending markets

💡 Tip: Turn this ON in strong trends, leave OFF in choppy markets for more signals.

Volume Filter (Optional - OFF by default)

Average Period: 20 bars

Surge Multiplier: 1.5x

When ON: Requires volume spike for signal confirmation

Use case: High-volume breakouts

💡 Tip: Enable this for crypto/stocks, disable for forex (lower volume reliability).

RSI Divergence Detection (Advanced)

Regular Divergences (Reversal Signals)

Regular Bullish: Price makes lower low, RSI makes higher low → Reversal UP

Regular Bearish: Price makes higher high, RSI makes lower high → Reversal DOWN

Line Color: Bright Light Blue (#00D9FF) - Solid lines

Meaning: Momentum is weakening, trend may reverse

Hidden Divergences (Continuation Signals)

Hidden Bullish: Price makes higher low, RSI makes lower low → Uptrend continues

Hidden Bearish: Price makes lower high, RSI makes higher high → Downtrend continues

Line Color: Purple (#9D4EDD) - Dashed lines

Meaning: Trend is healthy, expect continuation

Divergence Settings:

Pivot Lookback: 5 left, 5 right (sensitivity)

Max Lookback: 60 bars (how far back to compare)

Require Divergence: OFF by default (optional extra filter)

💡 Tip: Regular divergences are more reliable for reversals. Hidden divergences are great for trend-following entries.

📈 Visual Elements

Dynamic Bands (Envelope System)

Upper Band: Red line (resistance)

Lower Band: Green line (support)

Basis Line: Middle line (changes color with trend)

Green = Uptrend

Red = Downtrend

Yellow = Neutral

Cloud Fill: Shows trend strength

Green cloud = Bullish momentum

Red cloud = Bearish momentum

Info Panel (Top Right)

Displays real-time status of all indicators:

Fisher State (OVERSOLD/OVERBOUGHT/NEUTRAL)

RSI value

Volume status (SURGE/NORMAL)

ATR state (EXPANDING/CONTRACTING)

ADX value (color-coded: gray<15, orange 15-24, green>24)

Trend direction

DPO % (cycle position)

Regular Divergence status

Hidden Divergence status

💡 Tip: Watch the panel! When ADX turns green (>25) and RSI hits oversold/overbought, prepare for signals.

💡 Usage Tips & Best Practices

For Beginners:

Start with default settings - They work well across most markets

Keep ALL optional filters OFF initially - Get more signals to learn

Focus on ADX - Only trade when ADX > 20 (trending markets)

Use 15m-1H timeframes for day trading

Use 4H-Daily for swing trading

For Intermediate Traders:

Enable EMA Trend Filter - Cleaner signals in strong trends

Raise ADX threshold to 25 - Higher quality setups

Watch divergences - They add conviction to signals

Combine timeframes - Check 1H signals on 5m chart for entries

Adjust RSI levels for volatility:

Crypto: RSI 25/75 (more extreme)

Forex: RSI 30/70 (default)

Stocks: RSI 30/70 (default)

For Advanced Traders:

Enable Volume Filter for breakout confirmation

Enable "Require Divergence" for ultra-selective signals

Raise ADX threshold to 30 for only the strongest trends

Customize Fisher levels:

Aggressive: ±1.5

Conservative: ±2.5

Use multiple timeframes:

Check Daily for trend

Trade 1H signals

Enter on 15m pullbacks

Market-Specific Settings:

Crypto (High Volatility):

ATR Multiplier: 3.0-3.5

RSI: 25/75

ADX: 25

Volume Filter: ON

Forex (Trending):

ATR Multiplier: 2.5

RSI: 30/70

ADX: 20

EMA Filter: ON

Stocks (Balanced):

ATR Multiplier: 2.5

RSI: 30/70

ADX: 20

Volume Filter: ON (for breakouts)

Ranging Markets:

ATR Multiplier: 2.0

ADX: Keep at 20 but expect fewer signals

Disable EMA Filter

Focus on divergences

⚠️ Important Notes

What This Script Does Well:

✅ Catches momentum exhaustion reversals

✅ Filters out choppy, low-conviction trades

✅ Combines multiple confirmations

✅ Visual divergence detection

✅ Adaptive to market volatility

What This Script Doesn't Do:

❌ Predict the future (no indicator does)

❌ Work well in sideways/ranging markets (use ADX filter)

❌ Provide stop loss/take profit levels (you must decide)

❌ Guarantee profits (always use proper risk management)

Risk Management Tips:

Always use stop losses - Suggested: 1-1.5x ATR below entry

Position sizing - Risk 1-2% per trade maximum

Take profits - Consider 2-3x ATR targets

Don't force trades - Wait for all conditions to align

Avoid news events - Signals can fail during major news

🎯 Quick Setup Guide

Conservative Setup (Fewer, Higher Quality Signals):

ADX Threshold: 25-30

Enable: EMA Trend Filter

Enable: Volume Filter

Keep: Divergence optional

Balanced Setup (Default - Recommended):

ADX Threshold: 20

Disable: All optional filters

Let core logic work

Aggressive Setup (More Signals):

ADX Threshold: 15-18

Disable: All optional filters

Lower RSI thresholds: 35/65

📊 Alert System

The script includes comprehensive alerts:

🟢 BUY Signal - All conditions met

🔴 SELL Signal - All conditions met

⚠️ Setup Building - 4/5 conditions met (early warning)

📈 Market Trending - ADX crosses above threshold

📊 Market Ranging - ADX drops below threshold

💚 Regular Bullish Divergence - Reversal signal UP

❤️ Regular Bearish Divergence - Reversal signal DOWN

💙 Hidden Bullish Divergence - Uptrend continuation

💜 Hidden Bearish Divergence - Downtrend continuation

💡 Tip: Set up "Setup Building" alerts to prepare for signals before they trigger!

🏆 Pro Strategies

The Divergence Entry: Wait for regular divergence + signal arrow

The Trend Rider: Enable EMA filter, only trade with trend

The Breakout Hunter: Enable volume filter for explosive moves

The Patient Sniper: Enable ALL filters, take only perfect setups

Remember: The best traders wait for high-quality setups. Quality > Quantity! 🎯

Simple Grid Trading v1.0 [PUCHON]Simple Grid Trading v1.0

Overview

This is a Long-Only Grid Trading Strategy developed in Pine Script v6 for TradingView. It is designed to profit from market volatility by placing a series of Buy Limit orders at predefined price levels. As the price drops, the strategy accumulates positions. As the price rises, it sells these positions at a profit.

Features

Grid Types : Supports both Arithmetic (equal price spacing) and Geometric (equal percentage spacing) grids.

Flexible Order Management : Uses strategy.order for precise control and prevents duplicate orders at the same level.

Performance Dashboard : A real-time table displaying key metrics like Capital, Cashflow, and Drawdown.

Advanced Metrics : Includes Max Drawdown (MaxDD) , Avg Monthly Return , and CAGR calculations.

Customizable : Fully adjustable price range, grid lines, and lot size.

Dashboard Metrics

The dashboard (default: Bottom Right) provides a quick snapshot of the strategy's performance:

Initial Capital : The starting capital defined in the strategy settings.

Lot Size : The fixed quantity of assets purchased per grid level.

Avg. Profit per Grid : The average realized profit for each closed trade.

Cashflow : The total realized net profit (closed trades only).

MaxDD : Maximum Drawdown . The largest percentage drop in equity (realized + unrealized) from a peak.

Avg Monthly Return : The average percentage return generated per month.

CAGR : Compound Annual Growth Rate . The mean annual growth rate of the investment over the specified time period.

Strategy Settings (Inputs)

Grid Settings

Upper Price : The highest price level for the grid.

Lower Price : The lowest price level for the grid.

Number of Grid Lines : The total number of levels (lines) in the grid.

Grid Type :

Arithmetic: Distance between lines is fixed in price terms (e.g., $10, $20, $30).

Geometric: Distance between lines is fixed in percentage terms (e.g., 1%, 2%, 3%).

Lot Size : The fixed amount of the asset to buy at each level.

Dashboard Settings

Show Dashboard : Toggle to hide/show the performance table.

Position : Choose where the dashboard appears on the chart (e.g., Bottom Right, Top Left).

How It Works

Initialization : On the first bar, the script calculates the price levels based on your Upper/Lower price and Grid Type.

Entry Logic :

The strategy places Buy Limit orders at every grid level below the current price.

It checks if a position already exists at a specific level to avoid "stacking" multiple orders on the same line.

Exit Logic :

For every Buy order, a corresponding Sell Limit (Take Profit) order is placed at the next higher grid level.

MaxDD Calculation :

The script continuously tracks the highest equity peak.

It calculates the drawdown on every bar (including intra-bar movements) to ensure accuracy.

Displayed as a percentage (e.g., 5.25%).

Disclaimer

This script is for educational and backtesting purposes only. Grid trading involves significant risk, especially in strong trending markets where the price may move outside your grid range. Always use proper risk management.

NIFTY Options Breakout StrategyThis strategy trades NIFTY 50 Options (CALL & PUT) using 5-minute breakout logic, strict trend filters, expiry-based symbol validation, and a dynamic trailing-profit engine.

1️⃣ Entry Logic

Only trades NIFTY 50 options, filtered automatically by symbol.

Trades only between 10:00 AM – 2:15 PM (5m bars).

Breakout trigger:

Price enters the buy breakout zone (high of last boxLookback bars ± buffer).

Trend filter:

Price must be above EMA50 or EMA200,

AND EMA50 ≥ EMA100 (to avoid weak conditions).

Optional strengthening:

EMA20>EMA50 OR EMA50>EMA100 recent cross can be enforced.

Higher-timeframe trend check:

EMA50 > EMA200 (bullish regime only).

Start trading options only after expiry–2 months (auto-parsed).

2️⃣ One Trade Per Day

Maximum 1 long trade per day.

No shorting (long-only strategy).

3️⃣ Risk Management — SL, TP & Trailing

Includes three types of exits:

🔹 A) Hard SL/TP

Hard Stop-Loss: -15%

Hard Take-Profit: +40%

🔹 B) Step-Ladder Trailing Profit

As the option price rises, trailing activates:

Max Profit Reached Exit Trigger When Falls To

≥ 35% ≤ 30%

≥ 30% ≤ 25%

≥ 25% ≤ 20%

≥ 20% ≤ 15%

≥ 15% ≤ 10%

≥ 5% ≤ 0%

🔹 C) Loss-Recovery Exit

If loss reaches –10% but then recovers to 0%, exit at breakeven.

4️⃣ Trend-Reversal Exit

If price closes below 5m EMA50, the long is exited instantly.

5️⃣ Optional Intraday Exit

EOD square-off at 3:15 PM.

6️⃣ Alerts for Automation

The strategy provides alerts for:

BUY entry

TP/SL/Trailing exit

EMA50 reversal exit

EOD exit

Market Energy & Direction DashboardMarket Energy & Direction Dashboard - Daytrading

Overview

A comprehensive real-time market internals dashboard that combines NYSE TICK, NYSE Advance-Decline (ADD) momentum, VIX direction, and relative volume into a single visual traffic light system with intelligent signal synthesis. Designed for active daytraders who need instant confirmation of market direction and energy based on momentum alignment across all major internals.

What It Does

This indicator synthesizes multiple market internals using directional momentum analysis rather than static thresholds to provide clear, actionable signals:

• Traffic Light System: Single glance confirmation of market state

o Bright Green: Maximum bullish - all internals aligned (TICK + ADD rising + VIX falling + volume)

o Bright Red: Maximum bearish - all internals aligned (TICK + ADD falling + VIX rising + volume)

o Yellow: Exhaustion warning - TICK at extremes, potential reversal imminent

o Moderate Colors: Partial alignment - some confirmation but not complete

o Gray: Choppy, neutral, or conflicting signals

• Real-Time Dashboard displays:

o Current TICK value with exhaustion warnings

o Current ADD with directional momentum indicator (↑ rising = breadth improving, ↓ falling = breadth deteriorating, ± compression)

o VIX level with directional indicator (↓ declining = bullish, ↑ rising = bearish, ± compression = neutral)

o Relative volume (current vs 20-period average)

o Composite status message synthesizing all data into clear directional summary

Key Features

✓ Momentum-based analysis - all indicators show direction/change, not just levels ✓ Intelligent signal hierarchy from "Maximum" to "Moderate" based on internal alignment ✓ ADD directional momentum - catches breadth shifts early, works in all market conditions ✓ VIX directional analysis - shows if fear is increasing, decreasing, or stagnant ✓ Color-coded traffic light for instant decision making ✓ Detects TICK/ADD divergences (conflicting signals = caution) ✓ Exhaustion warnings at extreme TICK levels (±1000+) ✓ Composite status messages - "Maximum Bull", "Strong Bull", "Moderate Bull", etc. ✓ Customizable thresholds for all parameters ✓ Moveable dashboard (9 position options) ✓ Built-in alerts for all signal strengths, exhaustion, and divergences

How To Use

Setup:

1. Add indicator to your main trading chart (SPY, ES, NQ, etc.)

2. Default settings work well for most traders, but you can customize:

o TICK Extreme Level (default 1000)

o ADD Compression Threshold (default 100 - detects when breadth is stagnant)

o VIX Elevated Level (default 20)

o VIX Compression Threshold (default 2% - detects low volatility)

o Volume Threshold (default 1.5x average)

3. Position dashboard wherever convenient on your chart

Reading The Signals:

Signal Hierarchy (Strongest to Weakest):

MAXIMUM SIGNALS ⭐ (Brightest colors - All 4 internals aligned)

• "✓ MAXIMUM BULL": TICK bullish + ADD rising (↑) + VIX falling (↓) + Volume elevated

o This is the holy grail setup - all momentum aligned, highest conviction longs

• "✓ MAXIMUM BEAR": TICK bearish + ADD falling (↓) + VIX rising (↑) + Volume elevated

o Perfect storm bearish - all momentum aligned, highest conviction shorts

STRONG SIGNALS (Bright colors - Core internals aligned)

• "✓ STRONG BULL": TICK bullish + ADD rising (↑)

o Strong confirmation even without VIX/volume - breadth supporting the move

• "✓ STRONG BEAR": TICK bearish + ADD falling (↓)

o Strong confirmation - both momentum and breadth deteriorating

MODERATE SIGNALS (Faded colors - Partial confirmation)

• "MODERATE BULL": TICK bullish but ADD not confirming direction

o Proceed with caution - momentum present but breadth questionable

• "MODERATE BEAR": TICK bearish but ADD not confirming direction

o Proceed with caution - selling but breadth not fully participating

WARNING SIGNALS

• "⚠ EXHAUSTION" (Yellow): TICK at ±1000+ extremes

o Potential reversal zone - prepare to fade or take profits

o Often marks blow-off tops or capitulation bottoms

NEUTRAL/AVOID

• "CHOPPY/NEUTRAL" (Gray): Conflicting signals or low conviction

o Stay out or reduce size significantly

Individual Indicator Interpretation:

TICK:

• Green: Bullish momentum (>+300)

• Red: Bearish momentum (<-300)

• Yellow: Exhaustion (±1000+)

• Gray: Neutral

ADD (Advance-Decline):

• Green (↑): Breadth improving - more stocks participating in the move

• Red (↓): Breadth deteriorating - fewer stocks participating

• Gray (±): Breadth stagnant - no clear participation trend

VIX:

• Green (↓): Fear declining - healthy environment for rallies

• Red (↑): Fear rising - risk-off mode, supports downward moves

• Gray (±): Volatility compression - often precedes explosive moves

Volume:

• Green: High conviction (>1.5x average)

• Gray: Low conviction

Trading Strategy:

1. Wait for "MAXIMUM" or "STRONG" signals for highest probability entries

o Maximum signals = go full size with confidence

o Strong signals = good conviction, normal position sizing

2. Confirm directional alignment:

o For longs: Want ADD ↑ (rising) and VIX ↓ (falling)

o For shorts: Want ADD ↓ (falling) and VIX ↑ (rising)

3. Use exhaustion warnings (yellow) to:

o Take profits on existing positions

o Prepare counter-trend entries

o Tighten stops

4. Avoid "MODERATE" signals unless you have strong conviction from other analysis

o These work best as confirmation for existing setups

o Not strong enough to initiate new positions alone

5. Never trade "CHOPPY/NEUTRAL" signals

o Gray means stay out - preserve capital

o Wait for clear alignment

6. Watch for divergences:

o Price making new highs but ADD ↓ (falling) = distribution warning

o Price making new lows but ADD ↑ (rising) = potential bottom

o Divergence alert will notify you

Best Practices:

• Use on 1-5 minute charts for daytrading

• Combine with your price action or technical setup (support/resistance, trendlines, patterns)

• The dashboard confirms when to take your setup, not what setup to take

• Most effective during regular market hours (9:30 AM - 4:00 PM ET) when volume is present

• The strongest edge comes from "MAXIMUM" signals - wait for these for best risk/reward

• Pay special attention to ADD direction - it's the most predictive breadth indicator

• VIX compression (gray ±) often signals upcoming volatility expansion - prepare for bigger moves

Customization Option

All thresholds are adjustable in settings:

• TICK Extreme: Higher = fewer exhaustion warnings (try 1200-1500 for less sensitivity)

• ADD Compression Threshold: Change detection sensitivity

o Default 100 = balanced

o Lower (50) = more sensitive to small breadth changes

o Higher (200-300) = only shows major breadth shifts

• VIX Elevated: Adjust for current volatility regime (15-25 typical range)

• VIX Compression Threshold:

o Default 2% = balanced

o Lower (0.5-1%) = catches subtle VIX changes

o Higher (3-5%) = only shows significant VIX moves

• Volume Threshold: Lower for quieter stocks/times, higher for more confirmation

Alerts Available

• Maximum Bullish: All 4 internals aligned bullish (TICK + ADD↑ + VIX↓ + Volume)

• Maximum Bearish: All 4 internals aligned bearish (TICK + ADD↓ + VIX↑ + Volume)

• Strong Bullish: TICK bullish + ADD rising

• Strong Bearish: TICK bearish + ADD falling

• Exhaustion Warning: TICK at extreme levels

• Divergence Warning: TICK and ADD directions conflicting

Understanding the Signal Synthesis

The indicator uses intelligent logic to combine all internals:

"MAXIMUM" Signals require:

• TICK direction (bullish/bearish)

• ADD momentum (rising/falling) in same direction

• VIX direction (falling for bulls, rising for bears)

• Volume elevated (>1.5x average)

"STRONG" Signals require:

• TICK direction (bullish/bearish)

• ADD momentum (rising/falling) in same direction

• (VIX and volume are bonuses but not required)

"MODERATE" Signals:

• TICK showing direction

• But ADD not confirming or contradicting

• Weakest actionable signal

This hierarchy ensures you know exactly how much conviction the market has behind any move.

Technical Details

• Pulls real-time data from NYSE TICK (USI:TICK), NYSE ADD (USI:ADD), and CBOE VIX

• ADD direction calculated using bar-to-bar change with compression detection

• VIX direction calculated using bar-to-bar percentage change

• Volume calculation uses 20-period simple moving average

• Dashboard updates every bar

• No repainting - all calculations based on closed bar data

Who This Is For

• Active daytraders of stocks, futures (ES/NQ), and options

• Scalpers needing quick directional confirmation with multiple internal alignment

• Swing traders looking to time intraday entries with maximum confluence

• Volatility traders who monitor VIX behavior

• Market makers and professionals who trade based on breadth and internals

• Anyone who monitors market internals but wants intelligent synthesis vs raw data

Tips For Success

Trading Philosophy:

• Quality over quantity - wait for "MAXIMUM" signals for best results

• One "MAXIMUM" signal trade is worth five "MODERATE" signal trades

• Gray/neutral is not a sign of missing opportunity - it's protecting your capital

Signal Confidence Levels:

1. MAXIMUM (95%+ confidence) - Trade these aggressively with full size

2. STRONG (80-85% confidence) - Trade these with normal position sizing

3. MODERATE (60-70% confidence) - Only if confirmed by strong technical setup

4. CHOPPY/NEUTRAL - Do not trade, wait for clarity

Advanced Techniques:

• Breadth divergences: Watch for price making new highs while ADD shows ↓ (falling) = major warning

• VIX/Price divergences: Rallies with rising VIX (↑) are usually false moves

• Volume confirmation: "MAXIMUM" signals with 2x+ volume are the absolute best

• Compression zones: When both ADD and VIX show compression (±), expect explosive breakout soon

• Sequential signals: Back-to-back "MAXIMUM" signals in same direction = strong trending day

Common Patterns:

• Opening surge with "MAXIMUM BULL" that shifts to "EXHAUSTION" (yellow) = fade the high

• Selloff with "MAXIMUM BEAR" followed by ADD ↑ (rising) divergence = potential reversal

• Choppy morning followed by "MAXIMUM" signal afternoon = best trending opportunity

Example Scenarios

Perfect Bull Entry:

• Bright green signal box

• TICK: +650

• ADD: +1200 (↑)

• VIX: 18.30 (↓)

• Volume: 2.3x

• Status: "✓ MAXIMUM BULL" → ALL SYSTEMS GO - Take aggressive long positions

Strong Bull (Good Confidence):

• Green signal box (slightly less bright)

• TICK: +500

• ADD: +800 (↑)

• VIX: 19.50 (±)

• Volume: 1.2x

• Status: "✓ STRONG BULL" → Good long setup - breadth confirming even without VIX/volume

Caution Bull (Moderate):

• Faded green signal box

• TICK: +400

• ADD: +900 (↓)

• VIX: 20.10 (↑)

• Volume: 0.9x

• Status: "MODERATE BULL" → CAUTION - TICK bullish but breadth deteriorating and VIX rising = weak rally

Exhaustion Warning:

• Yellow signal box

• TICK: +1350 ⚠

• ADD: +2100 (↑)

• VIX: 17.20 (↓)

• Volume: 1.8x

• Status: "⚠ EXHAUSTION" → Take profits or prepare to fade - TICK overextended despite good internals

Divergence Setup (Potential Reversal):

• Faded green signal

• TICK: +300

• ADD: +1800 (↓)

• VIX: 21.50 (↑)

• Volume: 1.6x

• Status: "MODERATE BULL" → WARNING - Price rallying but breadth collapsing and fear rising = distribution

Perfect Bear Entry:

• Bright red signal box

• TICK: -780

• ADD: -1600 (↓)

• VIX: 24.80 (↑)

• Volume: 2.5x

• Status: "✓ MAXIMUM BEAR" → Perfect short setup - all momentum bearish with conviction

Compression (Wait Mode):

• Gray signal box

• TICK: +50

• ADD: -200 (±)

• VIX: 16.40 (±)

• Volume: 0.7x

• Status: "CHOPPY/NEUTRAL" → STAY OUT - Volatility compression, no conviction, await breakout

Performance Optimization

Best Market Conditions:

• Works excellent in trending markets (up or down)

• Particularly powerful during high-volume sessions (first/last hours)

• "MAXIMUM" signals most reliable during 9:45-11:00 AM and 2:00-3:30 PM ET

Less Effective During:

• Lunch period (11:30 AM - 1:30 PM) - lower volume reduces signal quality

• Low-volatility environments - compression signals dominate

• Major news events in first 5 minutes - wait for internals to stabilize

Recommended Use Cases:

• Scalping: Trade only "MAXIMUM" signals for quick 5-15 minute moves

• Daytrading: Use "MAXIMUM" and "STRONG" signals for position entries

• Swing entries: Use "MAXIMUM" signals for optimal intraday entry timing

• Exit timing: Use "EXHAUSTION" (yellow) warnings to take profits

________________________________________

Pro Tip: Create a dedicated workspace with this indicator on SPY/ES/NQ charts. Set alerts for "MAXIMUM BULL", "MAXIMUM BEAR", and "EXHAUSTION" signals. Most professional traders only trade the "MAXIMUM" setups and ignore everything else - this alone can dramatically improve win rates.

DEMA ATR Strategy [PrimeAutomation]⯁ OVERVIEW

The DEMA ATR Strategy combines trend-following logic with adaptive volatility filters to identify strong momentum phases and manage trades dynamically.

It uses a Double Exponential Moving Average (DEMA) anchored to ATR volatility bands, creating a self-adjusting trend baseline.

When the adjusted DEMA shifts direction, the strategy enters positions and scales out profit in phases based on ATR-driven targets.

This system adapts to volatility, filters noise, and seeks sustained directional moves.

⯁ KEY FEATURES

DEMA-Volatility Hybrid Filter

Uses Double EMA with ATR expansion/compression logic to form a dynamic trend baseline.

Directional Shift Entries

Entries occur when the adjusted DEMA flips trend (bullish crossover or bearish crossunder vs its past value).

Noise Reduction Mechanism

ATR range caps extreme moves and prevents false flips during choppy volatility spikes.

Multi-Level Take Profits

Targets scale out positions at 1×, 2×, and 3× ATR multiples in the trade direction.

Volatility-Adaptive Targets

ATR multiplier ensures profit targets expand/contract based on market conditions.

Single-Direction Exposure

No pyramiding; the strategy flips position only when trend shifts.

Automated Trade Finalization

When all profit targets trigger, the position is fully closed.

⯁ STRATEGY LOGIC

Trend Direction:

DEMA baseline is modified using ATR upper/lower envelopes.

• If the adjusted DEMA rises above previous value → Bullish

• If it falls below previous value → Bearish

Entry Rules:

• Enter Long when bullish shift occurs and no long position exists

• Enter Short when bearish shift occurs and no short position exists

Take Profit Logic:

3 partial exits for each trade based on ATR:

• TP1 = ±1× ATR

• TP2 = ±2× ATR

• TP3 = ±3× ATR

Profit distribution: 30% / 30% / 40%

Exit Conditions:

• Exit when all TPs hit (full scale-out if sum of all TPs 100%)

• Opposite trend signal closes current trade and opens new one

⯁ WHEN TO USE

Trending environments

Medium–high volatility phases

Swing trading and intraday trend plays

Markets that respect momentum continuation (crypto, indices, FX majors)

⯁ CONCLUSION

This strategy blends DEMA trend recognition with ATR-based volatility adaptation to generate cleaner directional entries and structured take-profit exits. It is designed to capture momentum phases while avoiding noise-driven false signals, delivering a disciplined and scalable trend-following approach.

Crypto Grid 2025+ Long Only (Asym TP)Crypto Grid 2025+ Long Only (Asymmetric Take-Profit) is a long-only mean-reversion grid strategy designed for intraday cryptocurrency trading.

The core idea is to accumulate long positions as price moves downward within a locally defined price range and to exit positions on upward retracements.

The strategy automatically builds a multi-level grid between the highest and lowest price over a user-defined lookback period (“range length”). Each grid level acts as a potential entry point when price crosses it from above.

Key Features

1. Long-only grid logic

The strategy opens long positions only, progressively increasing exposure as price moves into lower grid levels.

2. Asymmetric take-profit mechanism

Instead of taking profit strictly at the next grid level, the strategy allows targeting multiple levels above the entry point. This increases the average profit per winning trade and shifts the reward-to-risk profile toward larger, less frequent wins.

3. Optional partial take-profit

A portion of each trade can be closed at the nearest grid level, while the remainder is held for a more distant asymmetric target. This balances consistency and profit potential.

4. Volume-based market filter

Entries can be restricted to periods of healthy market activity by requiring volume to exceed a moving-average baseline.

5. Capital-scaled position sizing

Position size is determined by risk percentage, grid spacing, and a dynamic sizing mode (original / conservative / aggressive).

6. Built-in risk controls

global stop below the lower boundary of the range,

global take-profit above the upper boundary,

automatic shutdown after a configurable loss-streak.

Market Philosophy

This strategy belongs to the mean-reversion family: it expects short-term overshoots to revert back toward mid-range liquidity zones.

It is not trend-following.

It performs best in choppy, range-bound, or slow-grinding markets — especially on liquid crypto pairs.

Recommended Use Cases

Short timeframes (1–15 minutes)

High-liquidity crypto pairs

Sideways or rotational price action

Exchanges with low fees (due to higher order count)

Not Intended For

Strong trending markets without pullbacks

Assets with thin order books

Use with leverage without additional risk controls

Summary

Crypto Grid 2025+ Long Only (Asymmetric TP) is a refined grid-based mean-reversion strategy optimized for modern crypto markets. Its asymmetric take-profit framework is specifically engineered to reduce the classical issue of “small wins and large occasional losses” found in traditional grid systems, giving it a more favorable long-term trade distribution.

PivotBoss VWAP Bands (Auto TF) - FixedWhat this indicator shows (high level)

The indicator plots a VWAP line and three bands above (R1, R2, R3) and three bands below (S1, S2, S3).

Band spacing is computed from STD(abs(VWAP − price), N) and multiplied by 1, 2 and 3 to form R1–R3 / S1–S3. The script is timeframe-aware: on 30m/1H charts it uses Weekly VWAP and weekly bands; on Daily charts it uses Monthly VWAP and monthly bands; otherwise it uses the session/chart VWAP.

VWAP = the market’s volume-weighted average price (a measure of fair value). Bands = volatility-scaled zones around that fair value.

Trading idea — concept summary

VWAP = fair value. Price above VWAP implies bullish bias; below VWAP implies bearish bias.

Bands = graded overbought/oversold zones. R1/S1 are near-term limits, R2/S2 are stronger, R3/S3 are extreme.

Use trend alignment + price action + volume to choose higher-probability trades. VWAP bands give location and magnitude; confirmations reduce false signals.

Entry rules (multiple strategies with examples)

A. Momentum breakout (trend-following) — preferred on trending markets

Setup: Price consolidates near or below R1 and then closes above R1 with above-average volume. Chart: 30m/1H (Weekly VWAP) or Daily (Monthly VWAP) depending on your timeframe.

Entry: Enter long at the close of the breakout bar that closes above R1.

Stop-loss: Place initial stop below the higher of (VWAP or recent swing low). Example: if price broke R1 at ₹1,200 and VWAP = ₹1,150, set stop at ₹1,145 (5 rupee buffer below VWAP) or below the last swing low if that is wider.

Target: Partial target at R2, full target at R3. Trail stop to VWAP or to R1 after price reaches R2.